SEC & CFTC Enforcement Update

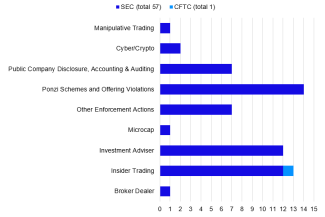

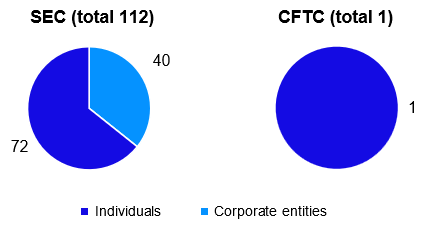

Between January and April 2026, the SEC filed 57 actions against a combined total of 112 defendants and respondents. (These figures exclude follow-on actions, bars, and suspensions.) There was one new CFTC action in this period.

Actions initiated by the SEC and CFTC in January, February, March and April 2026

Number of actions, by matter type

Types of defendants/respondents

Public company disclosures and accounting

SEC settles action against founder for concealing control of company and undisclosed related party transactions

SEC v. Shannon Illingworth and GP Solutions, Inc. (C.D. Cal., Jan. 8, 2026, Settled)

The SEC settled claims against a shipping container manufacturer and its founder for allegedly obscuring the founder’s control over the company, its primary clients, and other related parties.

In February 2020, the founder resigned as director of the manufacturing company. According to the SEC, he and his immediate family retained a majority of the manufacturer’s common stock and maintained sole control over the holding company that held all of the manufacturer’s Series A shares. The SEC alleged that the founder then attempted to conceal his control by enlisting friends and family members as titular officers, using the address of a nominal owner, and omitting the founder’s name from documents of incorporation.

In addition, between June 2020 and May 2022, the SEC claimed that the founder held control over seven private entities that did business with the manufacturer and provided the majority of the manufacturer’s revenue. During the relevant period, the manufacturer published 13 disclosures, including annual and quarterly statements. The SEC alleged that the manufacturer omitted any related party transactions disclosures and misled investors on the company’s dependence on related parties. Relatedly, the SEC alleged in its complaint that the founder had raised $11 million through one of his private entities by selling unregistered securities.

To settle the claims, the founder and manufacturer consented to the entry of a final judgment that imposed a civil penalty of $100,000 and a five-year officer-director bar and penny stock bar against the founder.

SEC litigation release | SEC complaint

SEC charges public company and former executives with alleged financial fraud in connection with SPAC merger

SEC v. Lawrence Anthony DiMatteo, Vadim Komissarov, Lottery.com, Inc., Matthew Clemenson, and Ryan Dickinson (S.D.N.Y., Jan. 22, 2026, Settled)

The SEC brought claims against a Texas-based company that sold lottery tickets, its former CEO, two of its former executives, and the CEO of a special purpose acquisition company (SPAC) for allegedly conducting a fraudulent scheme and making false statements in connection with a SPAC merger.

In 2020, the SPAC faced a regulatory deadline to complete the merger with the then privately held Texas company. The SEC claimed that, fearing financial losses if the SPAC dissolved, the SPAC CEO, with the participation of the Texas company’s executives, planned and executed a scheme to generate investor interest in the merger. According to the SEC, the group told investors that they earned $9 million from the sale of customer data and that the money would be used to purchase similarly valued assets. The SEC claimed, however, that the $9 million was a loan borrowed by a business partner and that the Texas company had used that money to overpay two businesses, which then returned the money to its source. The SEC further alleged that the Texas company executives told investors that the company engaged in a $30 million sale of advertising credits in the weeks prior to the SPAC merger when the credits were actually worth $10 million. Allegedly, the same counterparty involved in the $30 million sale was also involved in two additional bogus sales totaling more than $35 million following the merger. The SEC claimed that these scams accounted for most of the company’s purported revenue.

To settle the claims, the former executives agreed to pay disgorgement, prejudgment interest, and a civil penalty in an amount to be determined by the court. They also agreed to officer and director bars.

SEC litigation release | SEC complaint

SEC settles action against former executive and consultant for disclosure of false information

SEC v. Christopher B. Ferguson, and Brian P. McFadden (S.D.N.Y., Feb. 23, 2026, Settled)

The SEC settled claims against a former CEO of a company and a consultant to the company for alleged false public statements.

According to the SEC, the two individuals directed the company to issue a press release, which it attached to a Form 8-K, announcing it had secured approximately $7.5 million more in purchase orders than the actual amount secured. Three days before the press release, the individuals had allegedly negotiated with a distribution company for a $9 million sale of products, but the distribution company informed the individuals the next day that it was not proceeding with the order. The SEC alleged that the individuals continued revising the press release in anticipation of this order even after termination of negotiations. Following the alleged false press release, the SEC claimed that there was an increase of 197% in the company’s share price, and the consultant obtained illicit profits of approximately $75,208 after selling his shares.

To settle the claims, the individuals agreed to a civil penalty of $50,000 each and to a five-year officer and director bar. The consultant also agreed to a disgorgement of $75,208 with prejudgment interest of $28,209.

SEC litigation release | SEC complaint

SEC settles action against public company and two executives for accounting control failures

In the Matter of Key Tronic Corporation, Brett R. Larsen, and Nicholas S. Fasciana (A.P., Apr. 20, 2026, Settled)

The SEC settled claims against a public company, its former CFO (now CEO), and a senior vice president for alleged accounting control failures.

According to the SEC, between July 2020 and December 2020, employees at a company manufacturing facility in Minnesota generated false inventories in order to inflate the facility’s purported profitability. Specifically, the SEC alleges that employees falsely marked certain materials as undergoing manufacturing—even though no such manufacturing was ongoing—which had the effect of boosting the accounting value of the facility’s inventory. The senior vice president named in the order was allegedly aware of these practices and made no effort to stop them.

In January 2021, as the company was preparing to release its quarterly earnings report, company executives received an internal complaint about the alleged accounting improprieties at the Minnesota facility. The SEC alleged that executives immediately made adjustments to the company’s books and records. First, the SEC alleged that they reversed the improper invoices, thereby decreasing company income by approximately $1 million. Second, the SEC alleged that they corrected certain unrelated out-of-period (“OOP”) accounting errors, which increased income by approximately $764,000. According to the SEC, the executives did not conduct a proper materiality analysis before making the OOP adjustments. Furthermore, the SEC alleged that the executives released the quarterly report despite the advice of the company auditor to delay the release until the adjustments could be more thoroughly reviewed.

To settle the claims, all respondents agreed to the entry of a cease-and-desist order. In addition, the former CFO agreed to pay a civil penalty of $20,000 and the vice president agreed to pay a civil penalty of $15,000.

Insider trading

SEC settles action against former executive charged with insider trading

SEC v. Paul W. Jorgensen (S.D.N.Y., Mar. 16, 2026, Settled)

The SEC settled claims against the former Chief Revenue Officer of a digital platform provider for U.S. medical professionals for alleged insider trading.

According to the SEC, in August 2022, the executive sold company securities in advance of a quarterly earnings call announcing disappointing results. The sale was allegedly based on material nonpublic information regarding the company’s lower-than-expected sales. The SEC claimed the stock sales occurred outside of the company’s trading window for insiders and the executive neither pre-cleared his stock sales, nor reported the trading to the company’s General Counsel per company policy. The SEC further claimed that the executive failed to file required reports with the Commission publicly disclosing these sales.

In July 2023, the company informed the executive of his termination; however, the executive allegedly continued to receive confidential, nonpublic information about the company’s disappointing sales performance and a planned reduction in force. The SEC alleged that the executive again traded on the basis of material nonpublic information concerning the underperformance of the company’s sales team despite being subject to the Insider Trading Policy at the time of these trades. The executive’s alleged insider trading in August 2022 and August 2023 resulted in aggregate profits and losses avoided of approximately $2.5 million.

To settle the claims, the executive consented to the entry of a judgment in which he agreed to be permanently enjoined from violating federal securities law and permanently barred from serving as an officer or director of a public company. The SEC additionally seeks disgorgement, prejudgment interest, and/or a civil penalty. On January 9, 2026, the executive pled guilty to committing securities fraud in a parallel criminal case brought by the U.S. Attorney’s Office for the Southern District of New York.

SEC litigation release | SEC complaint

CFTC charges a U.S. service member with insider trading in a prediction market

CFTC v. Gannon Ken Van Dyke (S.D.N.Y., Apr. 23, 2026, Contested)

The CFTC brought claims against an active-duty service member in the U.S. Army for alleged insider trading.

From at least December 2025 through January 2026, the service member allegedly engaged in a fraudulent and deceptive scheme in connection with the purchase and sale of event contracts traded on a prediction market. In his capacity as an enlisted member of the U.S. Army’s Special Forces, he acquired sensitive nonpublic information regarding U.S. military operations to capture and arrest former Venezuelan President Nicolás Maduro and Cilia Flores. He was involved in the planning and execution of the operation. He is alleged to have breached his duty by misappropriating the information and using it to trade contracts related to Maduro on the prediction market. According to the CFTC, he generated more than $404,000 in profits through his trading.

The CFTC seeks restitution, disgorgement, civil monetary penalties, trading and registration bans, and a permanent injunction.

Investment adviser

SEC settles action against firm and executive for trade allocation practices

In the Matter of Barrington Asset Management, Inc. and Gregory David Paris (A.P., Feb. 10, 2026, Settled)

The SEC settled claims against an investment adviser and its executive for improper allocation of trades.

According to the SEC, from 2015 to 2019, the executive VP and chief compliance officer of the investment adviser executed trades through block trading omnibus accounts, allowing the execution of securities transactions without identifying in advance the specific individual account for which a trade was intended. The SEC alleged that the employee would allocate to his account a disproportionate share of trades that achieved gains on the first day but would allocate to his clients’ accounts a disproportionate share of trades that resulted in losses on the first day. In the firm’s brochures, the firm represented that no employee would “prefer his or her own interest to that of an advisory client” and the firm reviewed employee trading “on a regular basis.” The SEC claimed that the firm did not conduct any review of the executive’s trading and allocations.

To settle the claims, the executive agreed to pay a civil penalty of $40,000, disgorgement of $78,490, and prejudgment interest of $31,048.24. The executive further agreed to a six-month industry bar. The firm was censured.

SEC settles action against investment adviser for valuation-related practices

In the Matter of Madison Capital Funding LLC (A.P., Feb. 25, 2026, Settled)

The SEC settled claims against an investment adviser for selling loans to private fund clients without determining whether those trades were at fair market value, contrary to its disclosures to investors.

According to the SEC, the firm did not reasonably determine whether the trades to its private fund clients were at fair market value between March 2020 and May 2020 in accordance with its advisory agreements and disclosures to investors. The firm allegedly sold portions of certain senior loans it originated using funds from its parent company, which it typically held for 30 to 60 days, to these clients without determining the effect of the financial market disruption during the coronavirus pandemic on the fair market value of those loans. Although the firm increased monitoring and checked that loans maintained a B credit rating prior to sales, the SEC alleged that the firm made no additional analyses and that this was inadequate for checking fair market value due to price pressure from market disruption. Besides one, the loans sold during March 2020 and May 2020 either continue to perform or have been fully paid by the borrowers.

The firm had previously reimbursed more than $5 million to the funds after receiving a deficiency letter from the SEC’s Division of Examinations.

To settle the claims, the firm agreed to pay a $900,000 civil penalty.

Broker-dealer

SEC settles charges against broker-dealer for failing to file suspicious activity reports

In the Matter of Canaccord Genuity LLC (A.P., Mar. 6, 2026, Settled)

The SEC settled claims against a broker-dealer for its alleged failure to maintain a reasonably designed anti-money laundering (AML) program to surveil its equity trading activity.

According to the SEC, the broker-dealer’s compliance personnel routinely failed to monitor, identify, and investigate suspicious activity. When compliance staff did prepare internal AML exception reports identifying red flags, the SEC alleged that these reports, some of which went unreviewed for years at a time, often lacked critical information. The SEC further alleged that the broker-dealer’s written supervisory procedures did not provide adequate guidance on how to review suspicious activity beyond an instruction to examine “the totality of the circumstances.” In addition to the alleged lack of supervision by the AML Compliance Officer, certain employees allegedly falsified documentation in order to conceal the inadequacy of their reviews. As a result of these failures, the SEC estimated that the broker-dealer failed to file approximately 150 SARs between February 2019 and March 2022.

The broker-dealer agreed to pay a $20 million civil penalty as part of its settlement with the SEC.

Cyber/Crypto

SEC charges crypto founder and affiliated companies with allegedly defrauding investors

SEC v. Donald G. Basile, GIBF GP, Inc., and Monsoon Blockchain Corporation (A.P., Apr. 17, 2026, Contested)

The SEC charged a founder and two entities he controlled with allegedly perpetrating a securities offering fraud that raised approximately $16 million from hundreds of investors across the United States and abroad.

According to the SEC, the founder used materially false and misleading statements to offer and sell investors Simple Agreements for Future Tokens (“SAFTs”) as securities, which would give investors the rights to a crypto asset in the future. The alleged false claims included statements that the crypto asset was insured, that it was an asset backed cryptocurrency, and that its value was secured by an existing trust. He additionally claimed that 80% of the SAFT offering proceeds would flow back into the crypto asset to support the development of the token. Instead, the SEC alleges, the founder used accounts containing investor funds for personal benefits, including real estate purchases, credit card payments, and a horse.

The SEC seeks injunctive relief, disgorgement, prejudgment interest, civil penalties, and a conduct‑based injunction.

SEC litigation release | SEC complaint

Other enforcement actions

SEC settles charges against auditor for failing to properly audit mutual fund

In the Matter of EisnerAmper LLP (A.P., Mar. 6, 2026, Settled)

The SEC settled claims against an audit firm for its alleged failure to properly audit the 2020 financial statements of a mutual fund.

In an earlier June 2023 action, the SEC settled claims against the investment adviser to the mutual fund for mispricing the net asset value of its funds in an alleged overvaluation scheme. During this same period, the auditing firm reviewed the mutual fund’s financial statements and represented that the audits were conducted in accordance with PCAOB standards. The SEC, however, alleged that the audit firm had inaccurately concluded that the mutual fund’s financial statements fairly represented its financial position. According to the SEC, the audit firm had internally identified certain derivative instruments held by the mutual fund as carrying a high risk of misrepresentation, but it failed to properly scrutinize the fund’s valuation processes and controls. The SEC also claimed that the audit firm had an insufficient understanding of the mutual fund’s valuation process and did not exercise due professional care.

To settle the claims, the audit firm agreed to the entry of a cease-and-desist order and a censure.

Other announcements

New SEC Enforcement Director highlights Division priorities

On May 13, 2026, David Woodcock, the new Director of the SEC’s Division of Enforcement, delivered remarks outlining his guiding principles and areas of focus. Our client update on his speech may be found here. Director Woodcock endorsed Chairman Atkins’s “back-to-basics” approach, pledging to focus on the “fundamentals” of securities enforcement, including “offering frauds, accounting and disclosure fraud, insider trading, market manipulation, fraud by foreign actors targeting U.S. markets and investors, and breaches of fiduciary duties by [investment] advisers misusing client assets.” Director Woodcock additionally highlighted the Division’s focus on fraud rather than “honest mistakes.”

SEC updates Enforcement Manual

On February 24, 2026, the SEC’s Division of Enforcement announced updates to its Enforcement Manual. Our client update highlighting key changes is here. The Enforcement Manual updates included previously announced changes to the Wells process, delegation of authority for formal order, and requests for simultaneous consideration of waiver and settlement. Other updates concern efforts to improve transparency and efficiency, including new guardrails for converting a matter under inquiry to an investigation and additional guidance for closing investigations. The SEC also announced that the Enforcement Manual will undergo yearly review moving forward.

This communication, which we believe may be of interest to our clients and friends of the firm, is for general information only. It is not a full analysis of the matters presented and should not be relied upon as legal advice. This may be considered attorney advertising in some jurisdictions. Please refer to the firm’s privacy notice for further details.