Federal Reserve Proposes Stress Capital Buffer Requirements in Overhaul of CCAR

The Stress Buffer Requirements (SBR) Proposal would fundamentally restructure how the Federal Reserve’s stress testing and capital planning framework is used to impose capital requirements for large banking organizations. In general, the proposal would shift the quantitative capital requirements based on a firm’s pro forma stress losses, which currently are calculated and used only for purposes of the Federal Reserve’s Comprehensive Capital Adequacy Review (CCAR), into two new capital buffer requirements known as the stress buffer requirements.

The SBR Proposal would apply to BHCs with $50 billion or more in total consolidated assets, the U.S. intermediate holding companies of foreign banking organizations, and any nonbank systemically important financial institutions subject to supervisory stress testing (of which there are currently none). For the reasons explained below, U.S. global systemically important banking organizations (GSIBs) would be most affected by the SBR Proposal.

Proposed Stress Buffer Requirements

Under the SBR Proposal, the forward-looking supervisory stress test results calculated by the Federal Reserve once per year for the covered banking organizations would be integrated into these firms’ point-in-time capital requirements, which they must maintain throughout the year in order to avoid limitations on capital distributions and discretionary bonus payments. The stress buffer requirements include a stress capital buffer (SCB) requirement and a stress leverage buffer (SLB) requirement. Specifically, the stress buffer requirements would be calibrated to equal:

- the peak-to-trough decrease over the nine-quarter stress testing horizon in a firm’s standardized approach CET1 risk-based capital ratio (for the SCB) and in its tier 1 leverage ratio (for the SLB), in each case as determined under the severely adverse scenario of the Federal Reserve’s annual supervisory stress test; plus

- planned dividends over the fourth through seventh quarters of the planning horizon as a percentage of risk-weighted assets (for the SCB) or the denominator of the tier 1 leverage ratio (for the SLB).

The peak-to-trough decrease is measured by the difference between the starting level of the relevant capital ratio and the lowest level of that ratio under the severely adverse scenario in any of the nine quarters covered by the supervisory stress test. In the case of the SCB, the calibration would be the greater of (1) the peak-to-trough decrease in the firm’s CET1 risk-based capital ratio plus the applicable four quarters of planned dividends as a percentage of risk-weighted assets and (2) 2.5%. The resulting stress buffer requirements would be firm-specific and recalibrated annually based on the supervisory stress test.

1. The SCB Requirement

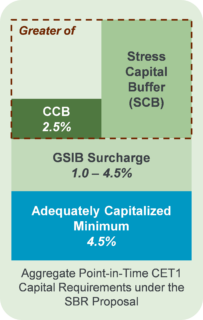

The SCB requirement would replace, for purposes of a firm’s capital requirements under the standardized approach, the static 2.5% capital conservation buffer requirement, but would not replace the GSIB surcharge or countercyclical buffer. As a result, the total standardized approach buffer requirement for a GSIB would equal the sum of:

- the stress capital buffer,

- the GSIB surcharge, and

- the countercyclical buffer (if deployed).

On a post-stress basis, a firm would be required to meet not only its minimum capital requirements to be adequately capitalized (i.e., a 4.5% CET1 risk-based capital ratio), but also the full amount of its GSIB surcharge to avoid any restrictions on capital distributions and discretionary bonus payments. This change is significant because a firm is currently required to have enough capital to absorb its peak-to-trough stress losses plus its planned capital distributions and meet its minimum capital requirements to be adequately capitalized (i.e., a 4.5% CET1 risk-based capital ratio) on a post-stress basis without needing to meet its GSIB surcharge.

The following graphic illustrates the aggregate standardized approach CET1 risk-based capital requirements under the SBR Proposal for a GSIB on a point-in-time basis, pursuant to the Federal Reserve’s capital rules, to avoid any restrictions on capital distributions or discretionary bonus payments.

For purposes of the advanced approaches, the buffer requirements would continue to consist of the current 2.5% static capital conservation buffer plus any applicable GSIB surcharge and any countercyclical buffer. This is consistent with the Federal Reserve’s existing approach of not using the advanced approaches to determine stress losses under CCAR.

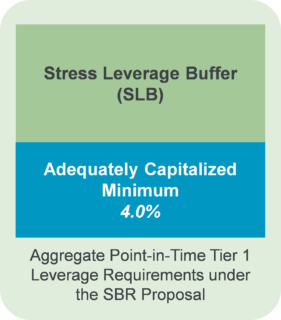

2. The SLB Requirement

The SLB requirement would not replace any existing buffer requirement in the point-in-time capital and leverage framework. As with the risk-based capital buffers, a firm would have to maintain the full amount of its SLB requirement on top of its 4% minimum required tier 1 leverage ratio in order to avoid limitations on capital distributions and discretionary bonus payments. Although this point-in-time leverage buffer requirement is new, it is consistent with the Federal Reserve’s current practice of evaluating a firm’s post-stress tier 1 leverage ratio under the existing quantitative CCAR requirements. There is no SLR component to the SLB requirement.

The following graphic illustrates the aggregate tier 1 leverage requirements under the SBR Proposal for a GSIB on a point-in-time basis, pursuant to the Federal Reserve’s capital rules, to avoid any restrictions on capital distributions or discretionary bonus payments.

Proposed Changes to Stress Testing and Capital Planning Assumptions

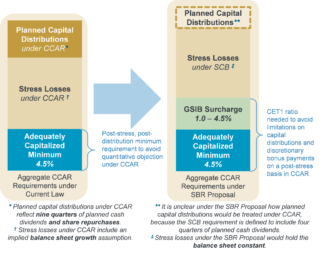

In addition to these structural changes, the SBR Proposal would also simultaneously relax certain assumptions related to the determination of a firm’s pro forma stress losses and its planned capital distributions for purposes of its capital plan in CCAR. These relaxed assumptions would have the effect of reducing the effective buffer that firms must maintain to “pre-capitalize” their planned capital distributions in their capital plans. They would also have the effect of eliminating the assumption of balance sheet growth over the stress testing horizon that is part of the current CCAR framework.

Specifically, in CCAR each firm would be required to assume its planned capital distributions for the fourth through seventh quarters of the planning horizon (corresponding to the one-year period beginning October 1 of the year of the capital planning cycle, coinciding with the effective date of its stress buffer requirements for the following one-year period) at a level consistent with any restrictions on capital distributions that would apply under the firm’s own baseline scenario projections.1 In addition, the firm would no longer be required to assume that it would continue share repurchases.

In view of the fact that the level of planned capital distributions would be based on a firm’s own baseline scenario and projections, the Federal Reserve has indicated that it intends to conduct periodic back-testing of these projections against realized results. If a firm’s realized results reflect a “pattern of materially underperforming baseline projections for earnings, capital levels or capital ratios,” the Federal Reserve may interpret such systematic underperformance as indicative of weakness in the firm’s capital planning and subject the firm to heightened scrutiny under any qualitative supervisory assessment of its capital planning processes.

The following graphic illustrates the proposed change in the amount of capital required to avoid limitations on capital distributions on a post-stress basis under CCAR.

Effect on CCAR

CCAR would remain under the SBR Proposal, but it would no longer be the primary mechanism for ensuring that large banking organizations maintain sufficient capital to continue operations through times of economic and financial stress. Instead, CCAR would be refocused to serve the purpose of estimating the firms’ stress losses and thereby determining the level of their SCB and SLB requirements. Under the proposal, the Federal Reserve would no longer be able to issue a quantitative objection to a firm’s capital plan, relying instead on the restrictions on capital distributions and discretionary bonus payments that apply under the capital rules if a firm fails to meet its full capital buffer requirements. However, the Federal Reserve would still be able to issue a qualitative objection for large and complex firms (generally, all GSIBs and all other BHCs with $250 billion or more in total consolidated assets or $75 billion or more in nonbank assets) and firms would continue to be required to describe their planned capital actions under CCAR and not exceed these planned distributions during the following year.

Effective Date, Timing and Procedural Considerations

The SBR Proposal would be effective on December 31, 2018, in time for the 2019 stress testing and capital planning cycle. Under the SBR Proposal’s timeline for stress testing and capital planning cycles, each firm’s stress buffer requirements would generally be released by the Federal Reserve by June 30 of the year of the cycle, take effect on October 1 of the same year and continue in effect until September 30 of the following year. We note that this one-year effective period for the annual stress buffer requirements matches the fourth through seventh quarters of the planning horizon under CCAR. Under this timeline, the first stress buffer requirements would become effective on October 1, 2019.

The SBR Proposal would revise or update several procedural considerations embedded in the existing CCAR process. Consistent with existing quantitative CCAR requirements, firms would have a one-time “mulligan” each cycle to resubmit planned capital actions within two business days of receiving an initial notice of its stress buffer requirements. This procedural safeguard allows a firm an opportunity to curtail planned distributions, if necessary to avoid any distribution limitations that would apply on a pro forma basis under its own baseline scenario projections. In addition, firms would be permitted to request a reconsideration of the calibration of either of its stress buffer requirements, triggering a requirement that the Federal Reserve respond in writing within 30 days, and would also be permitted to request a reconsideration of any qualitative objection to its capital plan.

Finally, among its numerous requests for comment on the SBR Proposal, the Federal Reserve specifically raised the possibility that the severely adverse scenario used for CCAR and stress testing purposes would be published for notice and comment. If adopted, this change would effectively allow firms to provide feedback to the Federal Reserve about the potential impact of the severely adverse scenario on their capital plans prior to the finalization of the annual CCAR instructions, and would clearly increase the transparency of the CCAR and stress testing framework.

1 These restrictions are determined by the most restrictive of the following requirements: (1) all standardized approach buffer requirements, including the SCB, (2) the SLB, (3) the eSLR (if applicable) and (4) the firm’s advanced approaches capital conservation buffer requirement (if applicable).

Law Clerk John O’Donnell contributed to this post.

This communication, which we believe may be of interest to our clients and friends of the firm, is for general information only. It is not a full analysis of the matters presented and should not be relied upon as legal advice. This may be considered attorney advertising in some jurisdictions. Please refer to the firm’s privacy notice for further details.