Federal Reserve and OCC Propose Tailoring of Enhanced Supplementary Leverage Ratios for GSIBs and their IDIs

The Federal Reserve and the OCC have proposed a rule that would recalibrate the enhanced supplementary leverage ratio (eSLR) requirements applicable to U.S. GSIBs and their insured depository institution (IDI) subsidiaries, and related requirements, by tailoring the eSLR levels to 50 percent of each firm’s GSIB surcharge. The proposal would make the eSLR requirements and related total loss absorbing capacity (TLAC) requirements for GSIB holding companies and the well-capitalized Prompt Corrective Action (PCA) framework for their IDI subsidiaries firm-specific and dynamic by tying them to a firm’s GSIB surcharge as calculated periodically under the Federal Reserve’s Basel III capital rule.

The proposal would only affect U.S. GSIBs and their IDI subsidiaries. Based on current GSIB surcharge levels, the proposal would reduce the eSLR and related requirements, particularly for IDI subsidiaries, reinforcing the status of the supplementary leverage ratio (SLR) as a backstop to the institutions’ applicable risk-based capital requirements.

The proposal does not specify a proposed effective date.

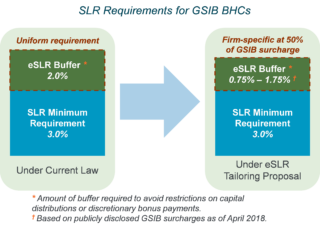

Recalibrated eSLR Buffer Requirement for GSIB BHCs

The eSLR Tailoring Proposal would recalibrate the uniform, static 2.0% eSLR requirement, applicable to the top-level BHC of a GSIB on a consolidated basis, with a firm-specific, dynamic buffer requirement calibrated at 50% of the firm’s risk-based GSIB surcharge. For example, a BHC firm with a GSIB surcharge of 3.0% would face a tailored eSLR requirement of 1.5%, down from the 2.0% eSLR requirement currently applicable to all BHCs.

Revised Well-Capitalized Standard for IDI Subsidiaries of GSIBs

The eSLR Tailoring Proposal would also recalibrate the current well-capitalized SLR standard under the PCA framework applicable to Federal Reserve- and OCC-supervised IDI subsidiaries of GSIBs. (There are currently no significant IDI subsidiaries of GSIBs for which the primary federal banking supervisor is the FDIC.) Specifically, it would change the well-capitalized standard from the uniform, static level of 6.0% to a firm-specific, dynamic level equal to the sum of (i) 3.0% and (ii) 50% of the GSIB surcharge applicable to the IDI’s top-tier parent BHC. For example, for a firm with a GSIB surcharge of 3.0% and an OCC-supervised national bank subsidiary, the national bank would be required to maintain an SLR of 5.5%, rather than 6.0%, to be considered well capitalized under OCC regulations. The well-capitalized standard is used for several regulatory purposes and has important knock-on effects, especially for BHCs that have elected to become financial holding companies (FHCs), as is the case with all eight U.S. GSIBs. FHCs and their IDI subsidiaries are required to be well capitalized and well managed to avoid restrictions or limitations on activities requiring FHC authority under the Bank Holding Company Act of 1956.

Corresponding Changes to TLAC

Finally, the eSLR Tailoring Proposal would make corresponding changes to the calibration of the TLAC leverage-based requirements applicable to GSIBs, as well as certain other technical changes to the TLAC rule. Specifically, the proposal would make the following substantive changes to the TLAC rule:

- TLAC SLR Buffer. Recalibrate the current TLAC SLR buffer requirement for GSIBs (currently 2% of total leverage exposures) with a buffer requirement equal to 50% of the firm’s GSIB surcharge (equivalent to the proposed recalibration of the eSLR buffer requirement discussed above).

- LTD SLR Minimum. Recalibrate the current LTD SLR minimum requirement for GSIBs (currently 4.5% of total leverage exposures) with a minimum requirement equal to the sum of (i) 2.5% and (ii) 50% of the firm’s GSIB surcharge.

- Actual Buffer Amount Formulas. Eliminate an existing discrepancy between the actual TLAC amount used in determining compliance with the minimum TLAC requirements and the formulas for measuring a firm’s applicable external TLAC buffer amount (including the risk-weighted and SLR buffers for GSIBs), which are used to determine compliance with the related TLAC buffer requirements, by amending the formulas for the buffer amount so that they add back 50% of the unpaid principal amount of outstanding LTD maturing between one and two years.

Requests for Comment

The SLR Tailoring Proposal includes several requests for comment, including three that we find particularly noteworthy:

- eSLR as Buffer for IDIs. The agencies requested comment on whether it would be more appropriate to apply the eSLR requirement to an IDI subsidiary of a GSIB as a capital buffer, in the same way as the eSLR requirement applies to GSIB BHCs, rather than as a requirement to be well capitalized.

- SLR Denominator. The agencies requested comments on alternative approaches to addressing the degree to which the SLR can act as a binding capital constraint, rather than as a backstop to the risk-based capital requirements. Specifically, the agencies asked about the possibility of excluding central bank reserves from the denominator of the SLR. Such a change would presumably apply to all banking organizations subject to the SLR (i.e., all advanced approaches banking organizations), not just GSIBs. This change would also go farther than the Senate Banking Bill, which would create a similar but more limited exclusion only for custody banks. In testimony before the House Financial Services Committee on April 17, 2018, Federal Reserve Vice Chair Randal Quarles noted that if the Senate Banking bill becomes law, the Federal Reserve and the OCC would have to consider how to calibrate the eSLR Tailoring Proposal so that the changes made by it and the Senate Banking Bill work together.

- TLAC SLR Minimum Requirement. The agencies also requested comment on the calibration of the TLAC SLR minimum requirement, asking whether the Federal Reserve should “modify the requirement … that a GSIB maintain an external loss-absorbing capacity amount that is no less than 7.5 percent of the GSIB’s total leverage exposure.” The invitation for comment on suggested modifications to the existing 7.5% minimum requirement—which is gold plated relative to the international standard—specifically asks whether the requirement should be modified to “better align… with similar foreign or international standards or expectations.”

Law Clerk John O’Donnell contributed to this post.

This communication, which we believe may be of interest to our clients and friends of the firm, is for general information only. It is not a full analysis of the matters presented and should not be relied upon as legal advice. This may be considered attorney advertising in some jurisdictions. Please refer to the firm’s privacy notice for further details.